December 2017 Energy Report

This email contains the month over month comparison of energy prices as well as the monthly commodity settlement prices. If you have any questions about your energy and waste portfolio or for an invoice and energy audits, price quotes for natural gas, electricity or waste, please contact RJ Consulting today.

Natural Gas and the end for 2017

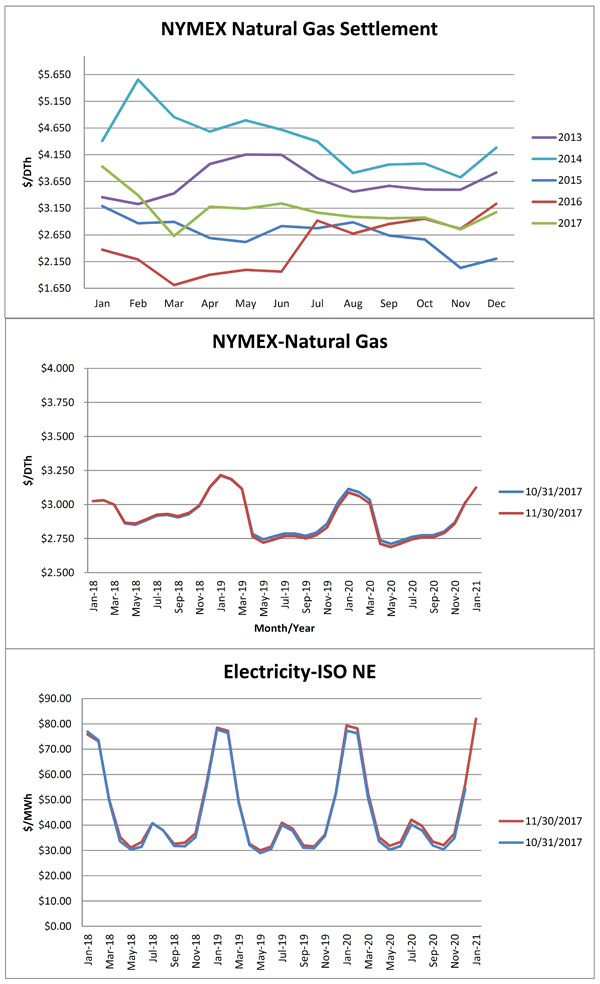

December 2017 settled at $3.074, up $0.32/Dth (11.7%) from November 2017 contract. December was the last natural gas contract for 2017 brings the 2017 natural gas average to $3.11/Dth, up $0.65/Dth (26.4%) from the 2016 average. The past two winters have been mild which has helped keep consumption down and underground storage full. Heading into the upcoming winter, the weather reports are mixed and let’s be honest; no one can predict the weather for the winter season. One potential problem for pricing I see is the first time in over three years we are going into winter below the five year average which from traders perspective can be considered a shortage and a reason to price gouge this winter. The past two winters we had storage over the five-year maximum average. The US is a major producer of natural gas which is good, and we are not drilling at our full capacity. Any gas price increase should get capped as higher priced gas will bring back more drilling and help meet winter demand. A cold winter will shake the gas market and make $3/Dth or lower gas a number for the history books, and a warm winter could send gas prices down to the $2.75/Dth range.

Peak Demand is Expensive

With commodity prices higher this year than last and everyone looking for ways to save on energy bills by installing solar panels and upgrading inefficient equipment which is all great measures, many are missing the impact demand has. As many turns for ways to generate their power, demand is not going away and is getting more expensive each year. Solar energy does nothing to reduce demand charges, and energy efficiency helps minimize equipment demand but operation and run times might limit this. Reducing demand is not an easy task and takes proper planning and data to understand how demand is set each month. Peak demand for electricity is usually set in 15 to 30-minute spikes within a billing cycle, and natural gas demand is typically the peak day usage traditionally set in the winter months. The utility companies have seen less revenue as more produce their power and efficiency uses less energy. The monopoly, I mean utility company can’t lose, so they are turning to demand to make up this revenue. RJ Consulting has and is going to offer more demand savings approaches for the company year as we want to put more control but in customer’s hands. Stay tuned as we plan to ring in 2018 with the power to save!

Please contact RJ Consulting if you would like to review your energy and waste portfolio. If you have any feedback or suggestions on the monthly emails, please share!

December 2017 Energy Report

![]()

If you have any questions or concerns about your current energy portfolio, please call or email to discuss.

Sincerely,

Roman Katynski, CEP

Energy & Waste Consultant, Owner

RJ Consulting LLC

An Energy and Waste Consulting Company