October 2017 Energy Report

This email contains the month over month comparison of energy prices as well as the monthly commodity settlement prices. If you have any questions about your energy and waste portfolio or for an invoice and energy audits, price quotes for natural gas, electricity or waste, please contact RJ Consulting today.

Natural Gas

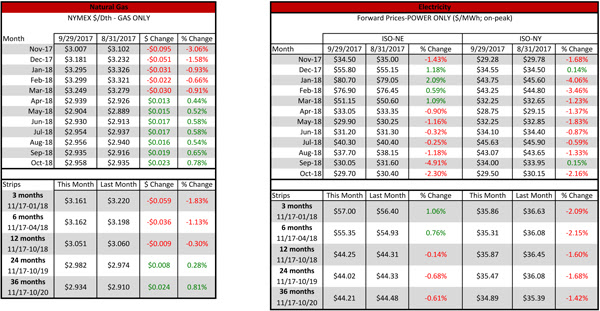

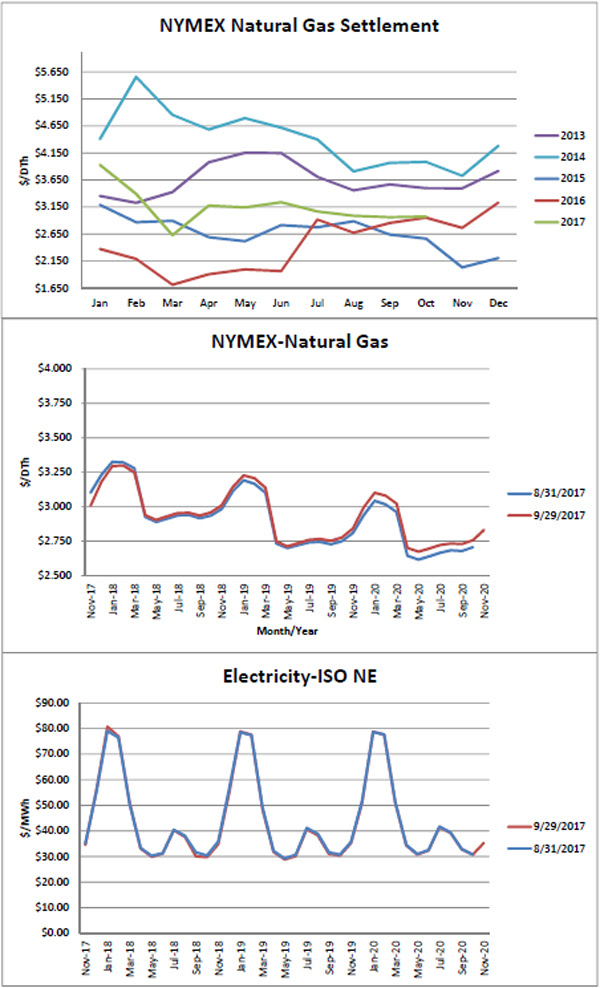

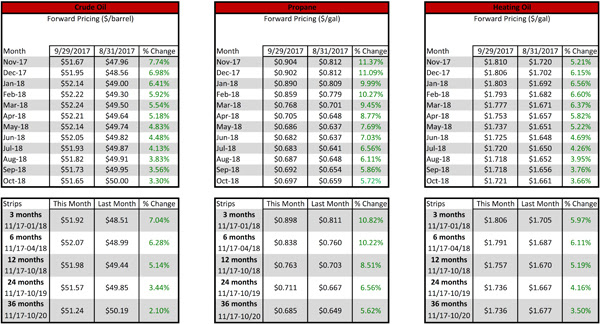

For the third month in a row, the settlement price for the promote month stayed below $3/Dth. The October 2017 contract settled at $2.974/Dth, up $0.013/Dth from the September 2017 contract. On the weather front, the first two weeks of October is looking warm. We can all thank the hot finish to September for that. The last two weeks were so hot; September is now expected to finish as the 5th warmest September since 2000; after a very chilly start. On the production front, last week storage gained 58/Bcf to settle at 3,466/Bcf. Stocks were 127/Bcf less than last year at this time and 41/Bcf above the five-year average of 3,425/Bcf. At 3,466/Bcf, total working gas is within the five-year historical range. Production is expected to keep trending higher towards year-end with October production to stall a bit as maintenance will cut some volumes, but the trend remains positive based on the forecasted temperatures. The current projection is a colder than normal winter for the US with cold temperatures reaching down as far as Northern Florida and parts of Texas. If an average cold winter hits the USA, we will see gas prices up hit the $4/Dth range by the beginning of 2018 and touch the $4.50/Dth by the beginning March 2018. My projection for the November 2017 settle is between $3.05/Dth to $3.25/Dth if the cold weather forecast holds. If it does not, November should say below $3/Dth.

Electricity

In 2016, about 4.08 trillion kilowatt hours (kWh) of electricity were generated at utility-scale facilities in the United States. About 65% of this electricity generation was from fossil fuels (coal-30.4% and natural gas-33.8%), about 20% was from nuclear energy, and about 15% was from renewable energy sources. Each year for the foreseeable future, the natural gas and renewable generation will continue to increase, and coal generation decrease. In the Northeast, on non-heating days, our natural gas-fired generation is over 65%. The current price of natural gas has helped keep electric prices stable. The problem over the next two years is the forward capacity market and potential natural gas price increases which will result in some higher electricity prices. The cost increases depending on your location as some areas are seeing much higher prices than normal. Many have reviewed and upgraded equipment to reduce electric consumption which will help manage price increases. Right now would be the time to review your facility to see what other opportunities might be available or to discuss electricity prices if you have a contract coming due within the next nine months.

Please contact RJ Consulting if you would like to review your energy and waste portfolio. If you have any feedback or suggestions to the monthly emails, please share!

October 2017 Energy Report

![]()

If you have any questions or concerns about your current energy portfolio, please call or email to discuss.

Sincerely,

Roman Katynski, CEP

Energy & Waste Consultant, Owner

RJ Consulting LLC

An Energy and Waste Consulting Company